Tell me if you’ve heard this one before. A client is in their mid 60s and retiring. 30 years ago they bought cash value life insurance, maybe from an agent who was a friend or from an insurance-focused financial advisor.

The client was promised to be able to use the cash values for retirement AND get the added benefit of a death benefit for their family, should they pass away in an untimely manner. The policy was set for lifetime premium payments, although your client was told that those premium payments could be offset by dividends and/or interest credits in the future should the client so choose.

There is a decent amount of cash in the policy, but nothing that is going to affect your client’s retirement one way or the other. Your client no longer needs the death benefit since his children are grown and they have more than enough retirement assets. The client also no longer desires to continue paying premiums into retirement.

Sound familiar? So what do you do?

If you don’t address the policy, then what will likely happen is that your client will just stop paying for the policy on their own and let the cash value be eroded by insurance charges. The only thing that saves that policy is their death, because ultimately those charges (and interest on policy loans) will eat up all of the cash value and the policy will lapse.

A better solution is to utilize that asset to check another necessary box on the client’s financial plan, long-term care.

Depending on the client’s age and health, there are several solutions available that would put them in a much better position: preserving that cash value, eliminating the premium payments, and providing tax-free leverage for long-term care needs.

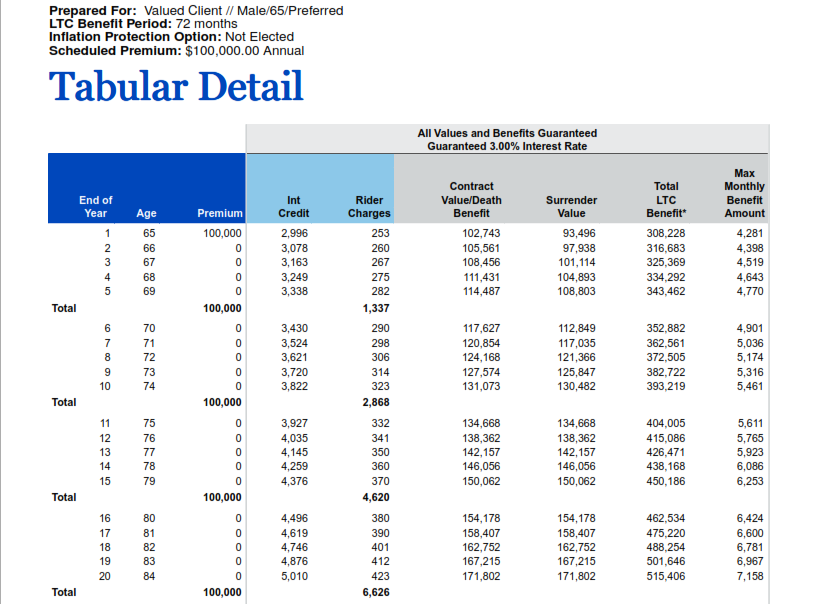

Let’s look at a few examples. Assume 250k death benefit with 100k in cash values.

Client 1: 65yo healthy male

This client is typically going to have the most leverage. A single healthy person can get an impressive amount of coverage on a 1035 from an existing policy.

Below, you’ll see that the death benefit is $123,850, which is roughly half of the original policy. BUT, the long-term care pool of money available at age 84 (a likely claim age) is $770,966. The internal rate of return, which is the return that one would need if they invested the initial 100k instead to use for long-term care purposes, is 9.78% after tax!

You can download the complete illustration HERE

Client 2: 75yo healthy female

Once a client reaches their 70s, products built on a life insurance chassis (see above) tend to be less attractive.

This is largely because the client is paying for both a life insurance policy and the long-term care coverage. Older clients will benefit from utilizing products built on an annuity chassis. Here, the death benefit is the initial premium plus interest minus charges (with the initial premium being the ultimate floor, fees won’t reduce the death benefit below the initial deposit). That allows the annuity carrier to offer substantial leverage towards long-term care.

Assuming continuing interest crediting, at age 84, the pool available for long-term care grows to $387,325. Even without growth, the guaranteed pool is $307,763, which is pretty strong leverage (3x+) for someone who hasn’t addressed long-term care protection in their mid-70s.

You can download the complete illustration HERE

Client 3: 65yo unhealthy male

Another advantage that the annuity-based long-term care hybrid products have is that they only underwrite for long-term care. Since many questions on a traditional or life hybrid application pertain to mortality, these products are much more flexible as it pertains to health.

For instance, here are the qualifying health questions from a major annuity hybrid carrier:

If your client can answer “no” to all of these questions, they’ll be approved.

There are a few additional questions to determine the amount of leverage, but the vast majority (80%+) qualify for the best possible leverage of 3x. Matched with a competitive guaranteed interest rate, at age 84 this client would have over 500k of total LTC benefits.

That is very valuable to someone who maybe had a heart attack or cancer 3 or 4 years ago.

You can download the complete illustration HERE

Client 4: 65yo healthy married couple

These are a little trickier, mainly because most of the “unneeded” life policies that we encounter are on a single life. The issue is that a 1035 must be like to like, meaning that we can’t go from a single ownership to joint.

The work around for this issue is to use a product that will still allow the 1035 but spread the tax liability over a period of time to allow for the second insured to be added.

While not as clean as the previous three examples, this strategy effectively funds a long-term care policy with a death benefit returning the majority of the initial premium should the funds go unused.

In this example, the 12,499.23 will be taxable with an exclusion ratio (using the basis and interest). After 10 years, the policy is fully funded, all taxes have been paid, and the policy has roughly 325k of available long-term care funds.

At age 84, that number balloons to north of $400,000, providing much-needed security, should either spouse encounter a long-term care event.

You can download the complete illustration HERE

No Other Options?

What if the person is so sick that they don’t qualify for any of the above? It happens where someone has a policy that they no longer wish to pay for, and yet their health is steadily declining. Or, they have a health condition like Parkinson’s, which hasn’t had a huge impact on their lives at this point but leaves them uninsurable through traditional means.

There are two directions that you can pursue, depending on the situation.

If the person is truly sick, but could live another few years, then considering a viatical or life settlement could make sense. This topic is beyond the scope of this article, but we can assist if that is something that your client is interested in. Often, the cash value is being eroded quickly, and the timing of the death/policy lapse is a coin flip. A settlement (selling the policy to a 3rd party) may be the best route to take.

If there is a health condition that has not yet become debilitating, but likely will be (like Parkinson’s), there is a guaranteed issue product available that will provide some immediate leverage towards long-term care. It will also allow for policy growth. This strategy has some tax benefits in addition to the preservation of the life policy’s cash value.

Conclusion

Considering the explosive sales of whole life and UL in the 80s and 90s, there are A LOT of these policies in force.

One important point, as an advisor, you probably won’t know about these policies unless you ask. Many folks have forgotten they have them and will just stop paying without your counsel, eventually lapsing the policy through the erosion of the cash values.

Have the discussion about long-term care. How are you planning to pay for it? What assets could we utilize to fund a 100k+/yr bill? A life policy with cash values that is no longer needed for either retirement or death benefit is the perfect funding vehicle to pay for this eventual cost. And, if using a hybrid, providing a benefit for your beneficiaries should there be no LTC need.

We’re here to help. Please feel free to reach out if you have a client with an unneeded life policy and we’ll design the perfect plan for their situation.