Ideally, your clients will have their long-term care planning complete by age 65. But, life happens, and sometimes clients either never get around to it, don’t understand how valuable it can be, or don’t qualify.

For those in their 70s, there are still several options available to them, mainly utilizing non-qualified funds or inherited IRAs. But what about your clients who are over the age of 80? From where and how will they fund a long-term care need?

Often, those clients own old annuities. Maybe they have been rolling a MYGA (multi-year guaranteed annuity) for years or they have an old non-qualified variable annuity that was originally going to be used for income that ended up not being needed.

If those annuities are earmarked for future care, then that’s a good start. There has been some planning done.

The downside is that often there is substantial gain that when tapped, will trigger income taxes at the worst possible time, when the client has very large long-term care expenses.

One option for these clients is to move these assets to a pension protected act (PPA) LTC compliant annuity.

Client Profile

Age: 81-87

Type: Existing non-qualified annuity with substantial gain

Objective: Desire to use that annuity for long-term care funding and eliminate the tax burden

How It Works

PPA compliant annuities allow for distributions to be tax free, regardless of how much of the contract is gain vs. basis.

Essentially, a client could move their existing annuity to a PPA compliant annuity and if used for long-term care, will NEVER have to pay the taxes on the gain.

While these annuities have been around for a while, the majority do not offer policies to people over the age of 80.

One of the top selling concepts at OneAmerica is to use their Annuity Care product as a receptacle for these annuities. Unlike the products available under age 80, the Annuity Care product does not offer any leverage for people older than 80, but does offer a competitive interest rate. At the time of this article, it provides a current rate of 3.45% on new deposits. As an added bonus, the LTC coverage grows at 3.95%.

That means that your client will have a bucket of money that is slightly larger if the funds are utilized for long term care. If not, then the death benefit will have still accumulated at the lesser rate.

Both rates are only guaranteed for the first year, however OneAmerica has been reasonable with renewals. The minimum contract guarantee for the accumulation bucket is 2% in year 2, whereas the minimum contract guarantee for the LTC bucket is 3.95% for the first 5 years and then 2% thereafter.

The primary reason for utilizing this strategy is to avoid taxation when the funds are used for LTC.

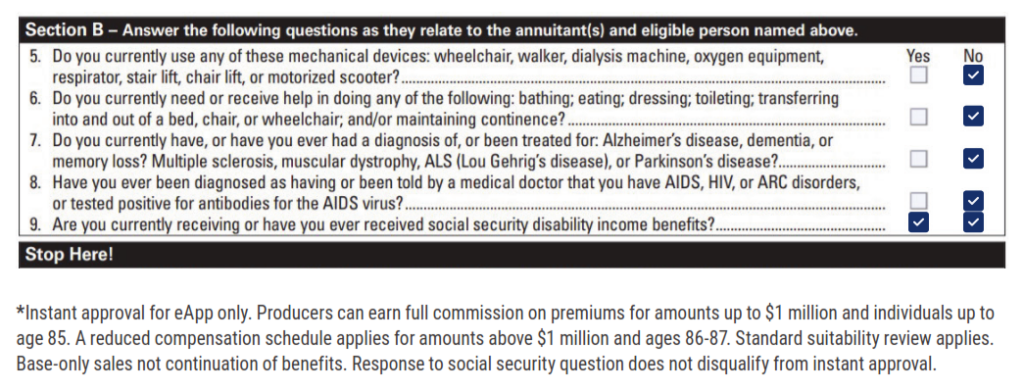

While there are health questions, they are very simple and the vast majority of applicants are approved. In most cases, the approval is instant. Below are the parameters for approval:

Once approved, the client will have a pool of money that can be used tax-free for long term care and if unused, will pass to a beneficiary.

Conclusion

People over 80 may have missed the boat for traditional long-term care coverage, however utilizing a PPA compliant annuity can help fund care without the extra tax bite.

As mentioned earlier, this is one of the top selling concepts at OneAmerica, largely because they’re the only game in town.

In having long-term care discussions with your older clients, ask if their existing annuity is a possibility for funding care. If it is, this concept will help provide that care in a more efficient manner, even when they’re over 80!

Reach out to us today if you have clients ages 81-87 who have non-qualified annuities that would be a likely source for long-term care expenses. It’s a very simple process and one that could save your clients thousands of dollars in taxes.